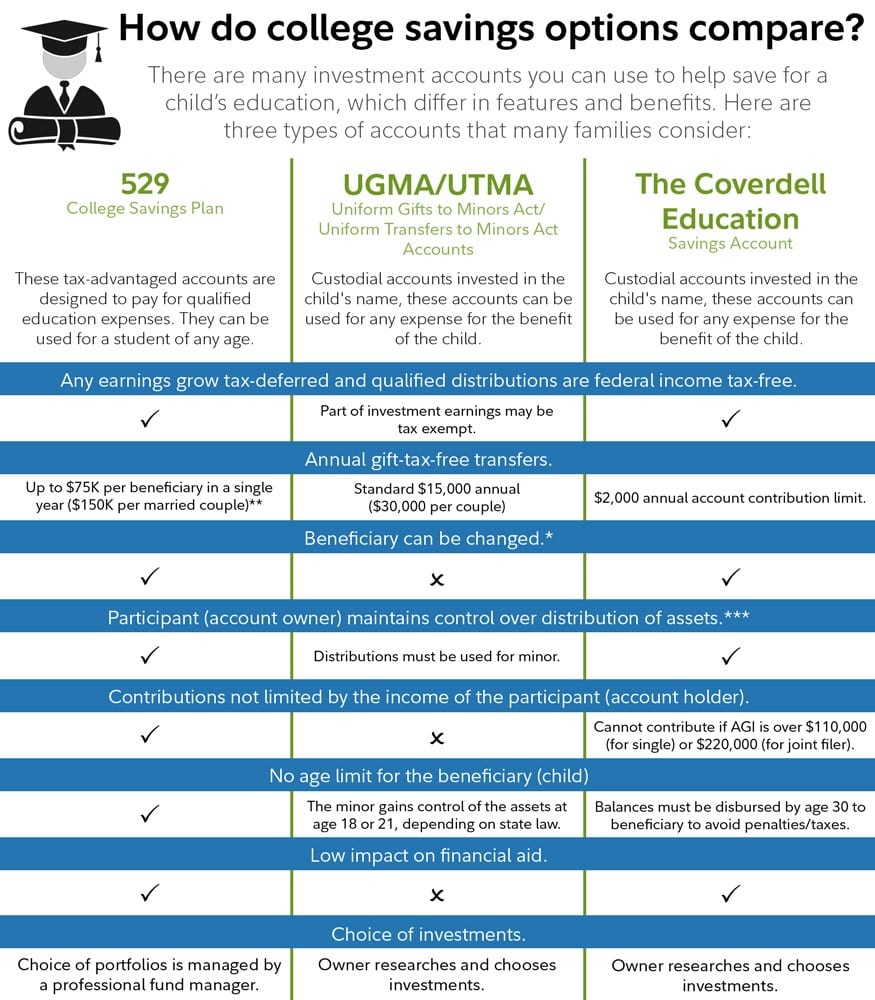

Key takeaways

✔ Alleviate the impact on financial aid

✔ Be more flexible thanks to fewer account restrictions

✔ Control the money and choose among many investment options

Why should you consider a 529 savings plan? The restrictions are few, and there are certain benefits, including certain tax advantages, potential minimal impact on the financial aid available to the student, and control over how and when the money is spent. What’s more? Now you are able to spend up to $10,000 per beneficiary per year on elementary or high school tuition expenses from a 529 plan.

A 529 savings account offers many advantages.

A 529 savings plan is a tax-advantaged account that allows for distributions to pay for tuition expenses at the elementary, high school, or college-level education and beyond. At the college or graduate level, funds from a 529 plan can be used for expenses such as tuition, fees, books, supplies, and any approved equipment the student may need to study at accredited institutions. In addition, you can take distributions for room and board, as long as the beneficiary of the plan is attending the school at least part time. When 529 funds are used for these qualified purposes, there is no federal income tax on investment gains (no capital gains tax, ordinary income tax, or Medicare surtax).

The ABCs of 529 plan benefits to consider:

Alleviate the impact on financial aid.

529 savings plan assets are considered parental assets and are factored into federal financial aid formulas at a This means that only up to 5.6% of the 529 assets are included in the expected family contribution (EFC) that is calculated during the federal financial aid process. That’s far lower than the potential 20% rate that is assessed on student assets, such as assets in an (custodial) accounts, which is are used to hold and protect assets for minors until they reach the age of majority in their state.

- Be more flexible.

In many ways, a 529 college savings plan has fewer restrictions than other college savings plans. These plans have no income or age restrictions and have no upper limit on annual contributions, unlike the Coverdell Education Savings Account (ESA), which limits contributions to $2,000 annually and restricts eligibility to those with adjusted gross income of $110,000 or less if single filers, and $220,000 or less if filing jointly.

Anyone can open and fund a 529 savings plan, parents, grandparents, other relatives and friends. You may even open one to pay for your own college expenses.

- Control the money and choose among many investment options.

With a 529 savings plan, the account owner (not the child) calls the shots on how and when to spend the money. Not only does this oversight keep the child from spending the money on something other than college, it allows the account owner to transfer the money to another beneficiary (e.g., a family member of the original beneficiary) for any reason.

For example, say the original child for whom the account was set up chooses not to go to college—or doesn’t use all the money in the account—the account owner can then transfer the unused money to another named beneficiary.

Want to learn more?

Both Fidelity and TIAA recommend that you take some time on the Saving for College website to view specific accounts available in your state.

- Helpful links from our partners

- TIAA 529 information, including links to FAQ and a handout on 529 options

- Fidelity’s overview of saving for college and qualifying withdrawals from a 529

- Prefer webinars? Listen to a pre-recorded webinar from a Fidelity 529 expert: http://www.brainshark.com/fidelityemg/college

Speak with your financial advisor, or meet with a Fidelity or TIAA consultant to help determine which education savings plan might be right for you. The important part is that you start planning now, to help save for the future.

TIAA: 888-381-8283 weekdays, 8 a.m. – 8 p.m. (EDT)

Fidelity: Chat with a representative or call 800-544-1914

1 Hurley, Joseph “Family Guide to College Savings” savingforcollege.com

Source: 1/19/2018: ABCs of a College Savings Plan

*For 529 accounts only, the new beneficiary must have one of the following relationships to the original beneficiary: 1) a son or daughter; 2) stepson or stepdaughter; 3) brother, sister, stepbrother, or stepsister; 4) father or mother or an ancestor of either; 5) stepfather or stepmother; 6) first cousin; 7) son-in-law, daughter-in-law, father-in-law, mother-in-law, brother-in-law, or sister-in-law; or 8) son or daughter of a brother or sister. The spouse of a family member (except a first cousin’s spouse) is also considered a family member. However, if the new beneficiary is a member of a younger generation than the previous beneficiary, a federal generation-skipping tax may apply. The tax will apply in the year in which the money is distributed from an account.

**In order for an accelerated transfer to a 529 plan (for a given beneficiary) of of $75,000 (or $150,000 combined for spouses who gift split) to result in no federal transfer tax and no use of any portion of the applicable federal transfer tax exemption and/or credit amounts, no further annual exclusion gifts and/or generation-skipping transfers to the same beneficiary may be made over the five-year period, and the transfer must be reported as a series of five equal annual transfers on Form 709, United States Gift (and Generation-Skipping Transfer) Tax Return. If the donor fails to survive the five-year period, a portion of the transferred amount will be included in the donor’s estate for estate tax purposes.

***For 529 savings plans, contributions are considered revocable gifts; owner controls the account; child is the beneficiary. For UGMA/UTMA accounts, contributions are considered irrevocable gifts; distributions must be used for minor; custodian controls the account until it is transferred to the minor at the age of majority. For Coverdell accounts, contributions are considered irrevocable gifts; account owner controls the account; child is beneficiary